Market Commentary January 2024

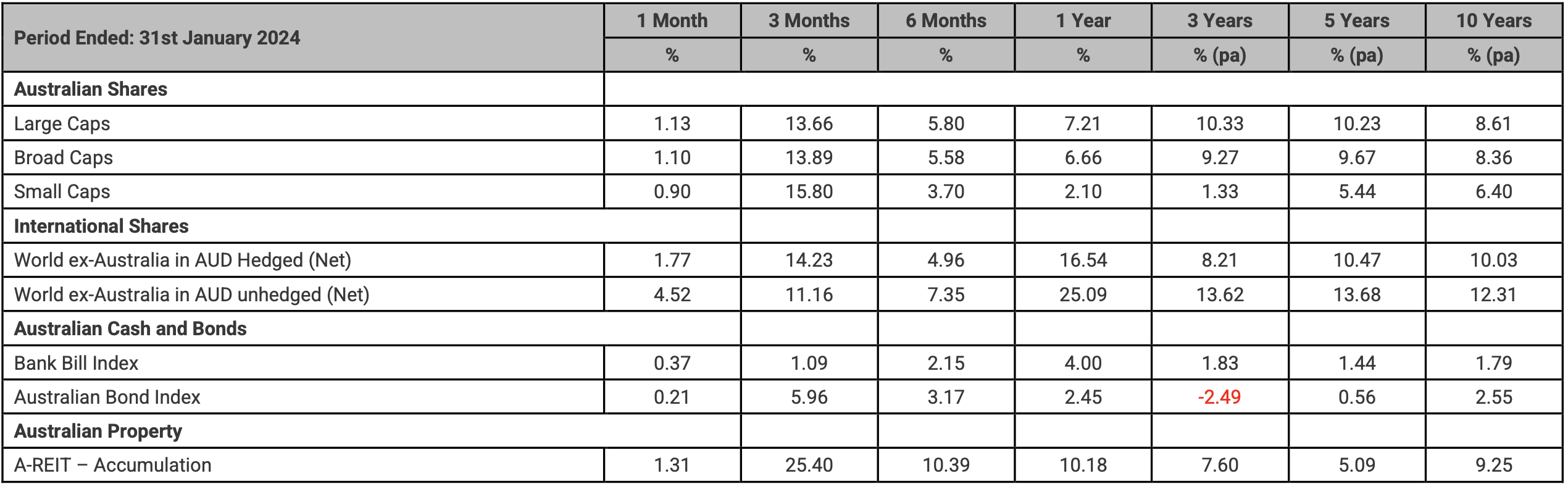

In January the US and Australian equity markets achieved new all-time highs delivering returns for the 12 months to 31st January in their local currencies of 20% and 7% respectively. US equities were lifted by the strength of the “Magnificent 7” labelled stocks being Microsoft, Meta Platforms, Tesla, Apple, Alphabet, Amazon, and NVIDIA. The rally in equities was driven by cooling inflation coupled with the expectation that a hard landing, i.e. a recession, will be avoided and that cash rate reductions will start to occur soon. Therefore, risks to equity returns going forward have lessened. Bond yields didn’t move significantly in January noting that in December yields fell significantly reflecting the future potential cash rate reductions due in 2024 and 2025.

The US Federal Reserve (FED) met in January and elected to maintain its current 5.25-5.5% cash rate setting. Despite low inflation in the US employment is still very strong. The market is expecting lower cash rates in 2024, however the FED needs to ensure that they do not create a second wave of higher inflation that will be even harder to tame. At the end of January the Australian Bureau of Statistics reported that inflation in Australia for the December 2023 quarter rose 0.6% and 4.1% annually. The Reserve Bank of Australia (RBA) did not meet in January.

Australian large cap Equities rose by 1.1% driven by the Energy sector and Financials (both up ~5%) whilst the Material sector fell by ~5%). Hedged global equities rose by 1.8% whilst unhedged global equities rose by 4.5%, as the Australian dollar weakened by 4% in the month to US$0.6565.

The Australian 10-year government bond yield increased by 12bps to 4.07% and the 2-year government bond yield increased by 4bps to 3.75%. The US 10-year government bond yield rose by 16bps to close at 4.04% and the US 2-year government bond yield fell by 4bps to 4.21%.

KEY DEVELOPMENTS POST MONTH-END

The RBA met on the 6th February and elected to retain the current cash rate at 4.35% noting that “While there are encouraging signs, the economic outlook is uncertain and the Board remains highly attentive to inflation risks. The central forecasts are for inflation to return to the target range of 2-3 per cent in 2025, and to the midpoint in 2026”.

Benchmark Returns

Article source: Personal Financial Services Ltd (PFS)

Disclaimer: Research Insights is a publication of Personal Financial Services Limited ABN 26 098 725 145 (PFS). Any advice in this article is general advice only and does not take into account the objectives, financial situation or needs of any particular person. It does not represent legal, tax or personal advice and should not be relied on as such. You should obtain financial advice relevant to your circumstances before making product decisions. Where appropriate, seek professional advice from a financial adviser. Where a particular financial product is mentioned, you should consider the product disclosure statement before making any decisions in relation to the product and we make no guarantees regarding future performance or in relation to any particular outcome. Whilst every care has been taken in the preparation of this information, it may not remain current after the date of publication and Personal Financial Services Ltd (PFS) and its related bodies corporate make no representation as to its accuracy or completeness.

{kind=link}