Market Commentary September 2020

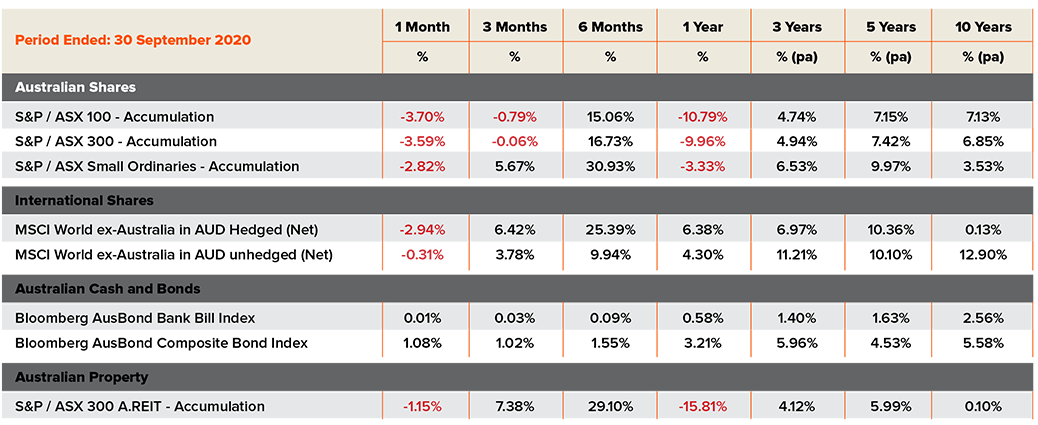

Growth assets declined in September. Investors adopted a more cautious stance due to a number of factors such as: The acceleration of COVID-19 cases globally, particularly the rise in the northern hemisphere; the lack of further stimulus or bond buying programs announced by central banks; and uncertainty around the US Presidential election on 3rd November.

Australia’s unemployment rate surprisingly fell to 6.8% from 7.5% in August. Without the Government’s JobKeeper program the unemployment rate would likely exceed 10% however with COVID-19 being contained and Victorian infection numbers falling hopefully “normality” can be resumed by November. We expect the biggest impacts to the economy will be from overseas tourists and international students , and on industries such as agriculture and viticulture that rely on the “backpacking” workforce.

The Australian equity market erased the gains of July and August and fell 3.6% in September with the Financial, Information Technology and Energy sectors amongst the worst performing sectors. During the month Westpac Banking Corporation agreed to pay the largest fine in Australian corporate history – a $1.3 billion civil penalty for 23 million breaches of anti-money laundering laws.

Technology stocks globally saw a rare period of profit taking with the technology heavy NASDAQ Composite Index in the US falling 5.2% in September. This was replicated in Australian technology stocks with the local Information Technology sector falling by 6.4% for the month. International equities fell by 2.9% on a currency-hedged basis while a lower AUD (down 3% against the USD to close at US$0.717) helped lessen the losses for unhedged investors to -0.3% for the month.

The RBA left interest rate and other policy settings on hold at their October 6th meeting however a rate cut to bring the cash rate down from 0.25% to 0.10% is highly anticipated at their November policy meeting. The Australian yield curve fell in August with the 10-year government bond yield falling by 20bps to 0.78% whilst the 2-year government bond yield fell by 9bps to 0.16% in anticipation of an imminent RBA interest rate cut. In the US the 10-year government bond yield fell 3bps to close at 0.68% and the 2-year government bond yield was flat at 0.13%.

Quick Budget Snapshot

- Infrastructure investment of an additional $7.5bn across all states/territories

- A range of targeted investment measures to support industry and businesses and help them to recover from the last 6 months

- For business with turnover up to $5bn there is an immediate deduction on capital assets acquired and they will also be able to offset losses against previous taxed profits

- Personal income tax reductions potentially back dated to take effect 1 July 2020

Article source: Australian Unity

Important Information: This article is a publication of Australian Unity Personal Financial Services Limited ABN 26 098 725 145 (AUPFS), AFSL 234459. Its contents are current to the date of publication only, and whilst all care has been taken in its preparation, AUPFS accepts no liability for errors or omissions. The application of its contents of specific situations (including case studies and projections) will depend upon each particular circumstance. This publication is general in nature and has been prepared without taking into account the objectives or circumstances of any particular individual or entity. It cannot be relied upon as a substitute for personal financial, taxation, or legal advice. This article was produced on 08 October 2020. © Copyright 2020

{kind=link}