Market Update March 2022

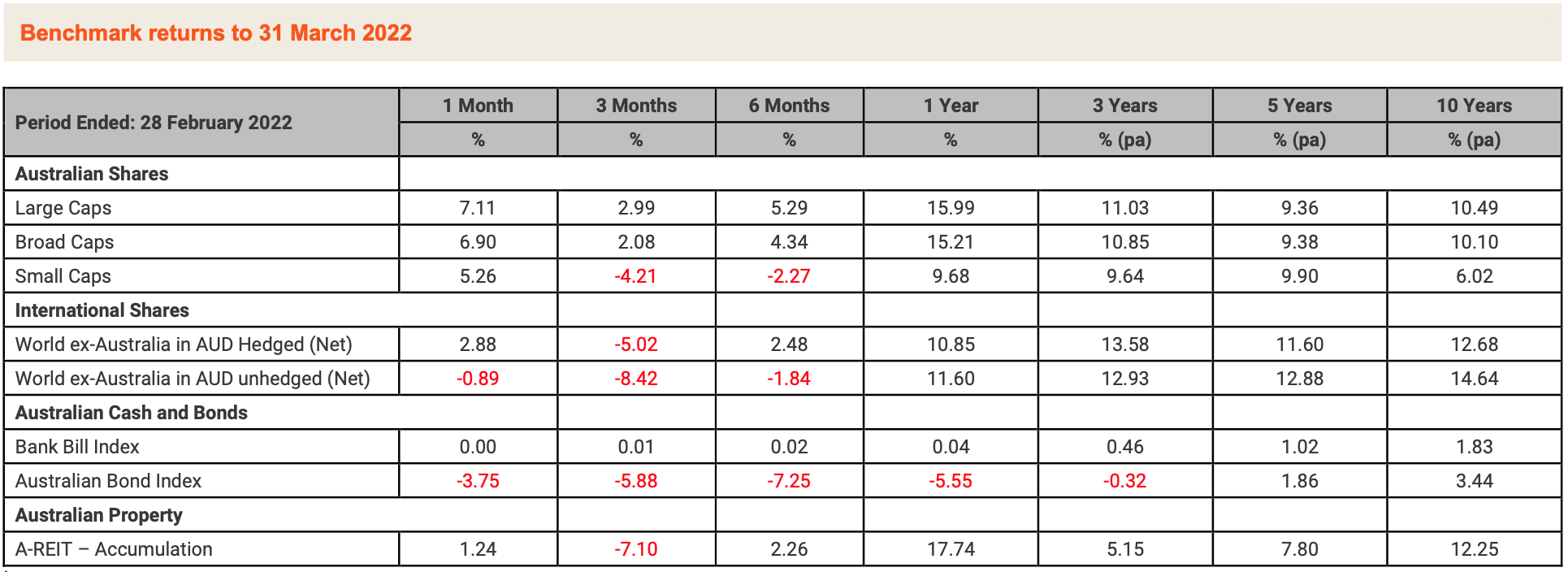

March provided a wide range of returns across asset classes. Rising inflation, the escalating conflict between Russia and Ukraine, COVID-19 related lockdowns in China and the US Federal Reserve’s much- anticipated official cash rate increase all influenced investment markets. Equity investors outside Europe adopted a “risk-on” stance which saw the Australian equity market gain 6.9% for the month and US shares return +3.6%. Stronger performing sectors in the Australian market included the Financials sector which benefitted from rising bond yields. The Energy and Materials sectors both gained as commodity prices remained buoyant. In the US the technology heavy NASDAQ index finish March ~13% above its intra-month low as investors moved to “buy the dip”.

International Equities were up 2.9% during the month whilst a rising Australian dollar, up 3.4% buying US$0.7496, resulted in negative returns (-0.9%) for unhedged international equity investors. Despite increased volatility since December, international equities have provided investors with double-digit returns over the past 12 months. Australian equities have outperformed international equities in the last year although returns over a longer time frame have lagged international equities. Interestingly, passive fixed income has failed to shield investors from market volatility in the past year with a return of -5.6%.

The US Federal Reserve raised interest rates for the first time since 2018 to a target rate of 0.25-0.50% with a hawkish rhetoric (i.e. more rate rises to come soon, and potentially of greater magnitude) in a bid to curb inflation which is running at a 40-year high of 7.9% for the year to February 2022. Bond yields across multiple maturity dates have lifted significantly and in the US some parts of the yield curve have become “inverted” – a situation whereby shorter-term debt has higher yields than longer term debt. Historically, yield curve inversion can be a precursor to a recession. However, in this instance the yield curve inversion reflects the bond market’s anticipation of sharp increases in the US Fed Funds rate in an effort to quell demand and temper inflation, and a view that this course of action will be successful in re-establishing longer-term inflation at lower levels.

Australian government bond yields moved higher in March with the Australian 10-year government bond yield increasing by 70bps to 2.84% and the 2-year government bond also rising by 70bps to 1.80%. US yields also rose, with the 10-year government bond yield gaining 51bps to close at 2.34% and the 2-year government bond yield increasing by 90bps to 2.33%.

Article source: Australian Unity

Important Information: Research insights is a publication of Australian Unity Personal Financial Services Limited ABN 26 098 725 145 (AUPFS). Any advice in this article is general advice only and does not take into account the objectives, financial situation or needs of any particular person. It does not represent legal, tax or personal advice and should not be relied on as such. You should obtain financial advice relevant to your circumstances before making product decisions. Where appropriate, seek professional advice from a financial adviser. Where a particular financial product is mentioned, you should consider the product disclosure statement before making any decisions in relation to the product and we make no guarantees regarding future performance or in relation to any particular outcome. Whilst every care has been taken in the preparation of this information, it may not remain current after the date of publication and Australian Unity Personal Financial Services LTD (AUPFS) and its related bodies corporate make no representation as to its accuracy or completeness.

{kind=link}