Market Commentary August 2020

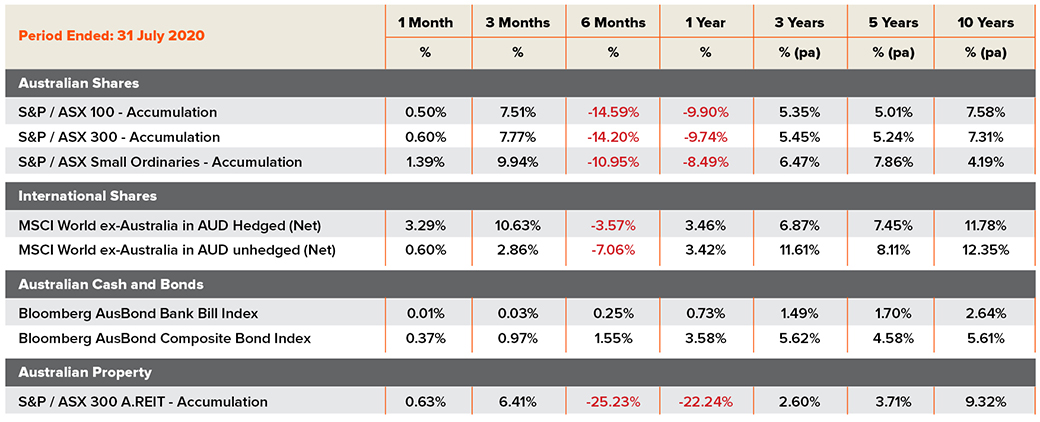

July was a relatively flat month for growth assets. Standout returns were achieved on hedged international equities as the Australian dollar continued to strengthen, a thematic over the last 3 months which now sees almost identical returns across hedged and unhedged equities over the past 12 months. The Australian dollar‘s recent appreciation is mostly against the US dollar, and partly reflects the buoyancy of the iron ore price (supported by central bank growth stimuli and supply constraints) plus the favorable interest rate differential between the US at zero and Australia at 0.25%. The US Dollar Index – a measure of the value of the US dollar relative to the currencies of a basket of the United States’ major trading partners – fell 4.15% during July.

US second-quarter GDP figures were released in July. These saw the US economy fall at an annual rate of 32.9%. It appears that US activity has weakened into the September quarter; for the week ending 25th July a further 1.434 million people in the US filed for initial unemployment insurance.

In Australia, the unemployment rate in June rose to a 22 year high of 7.4%. In addition, Australia’s CPI for the June quarter fell 1.9% with falls in childcare (-95%) and automotive fuels (-19.3%) leading the decline. An increase in COVID-19 cases across the globe along with further restrictions being applied with businesses closing potentially points to a “U” or an “L” shaped recovery rather than the “V” shaped recovery that was initially expected. Central banks globally have signaled continued stimulus to ensure economies will be propped up and therefore interest rate expectations remain muted.

The Australian equity market gained 0.6% for the month with the Technology and Communication Services sectors the strongest contributors to performance whilst the Health Care and Industrials sectors were two of the poorer performing sectors for July. The ASX Small Ordinaries rose by 1.4% for the month boosted by a strong gold sector which responded to an 11.9% gain in the US dollar denominated gold price to US$1,194 per ounce. Australian listed property returned 0.6% in July. Unhedged international equities rose by 0.6%, whilst a higher AUD (up 3.7% against the USD to close at US$0.7143) helped hedged international equities return 3.3% in July. US equities, as measured by the S&P500, were up over 5% led by the strong earnings updates from the FAANG stocks.

The Australian yield curve flattened slightly in July with the 10-year government bond yield falling by 5.5bps to 0.82% whilst the 2-year government bond yield lifted by 2bps to 0.27%. In the US both the 10-year and 2-year government bond yields fell, the 10-year by 13bps to close at 0.53% and the 2-year by 6bps to close at 0.11% noting that the US Federal Reserve base rate remains at zero.

Benchmark Returns 31 July 2020

Article source: Australian Unity

Important Information: This article is a publication of Australian Unity Personal Financial Services Limited ABN 26 098 725 145 (AUPFS), AFSL 234459. Its contents are current to the date of publication only, and whilst all care has been taken in its preparation, AUPFS accepts no liability for errors or omissions. The application of its contents of specific situations (including case studies and projections) will depend upon each particular circumstance. This publication is general in nature and has been prepared without taking into account the objectives or circumstances of any particular individual or entity. It cannot be relied upon as a substitute for personal financial, taxation, or legal advice. This article was produced on 07 August 2020. © Copyright 2020

{kind=link}