Aged 65+ and downsizing? A new rule could save you tax.

From 1 July 2018, people aged 65 and over will be able to sell their main residence and then make a ‘downsizer’ contribution into superannuation of up to $300,000 from the sale proceeds of their main residence.

Both members of a couple can take advantage of this measure, allowing a total amount of $600,000 to be contributed to superannuation per couple.

This new rule trumps other current rules which prevent many over-65s from making contributions to superannuation (such as the work test, the age 75 limit, and the $1.6 million balance test).

Why is this a good initiative for these people?

Because being allowed to contribute this money into superannuation means it can be invested and then earn income with little or no tax liability.

For example, if $600,000 was invested inside superannuation and earned, say, 5% p.a., that $30,000 income would be tax free for most people aged 65+ (assuming their finances were correctly set up).

Some points to be aware of:

- This rule only applies to principal places of residence that have been held for at least 10 years.

- The contribution must be made within 90 days of change of ownership and the superfund trustee must be notified it is a downsizer contribution at the time it is made.

- Although termed ‘downsizer’ contributions, there is no requirement to purchase a new residence.

- If your ‘total superannuation balance’ is above $1.3 million, it might be useful to make other planned contributions to superannuation prior to making a downsizer contribution. This is because, unlike other contributions, a downsizer contribution is allowed even if it results in an excess i.e. above $1.6 million.

- For some people, there may be significant Centrelink and Aged Care implications – both positive and negative – in regards to the downsizer strategy, and we strongly recommend that these people seek professional financial advice.

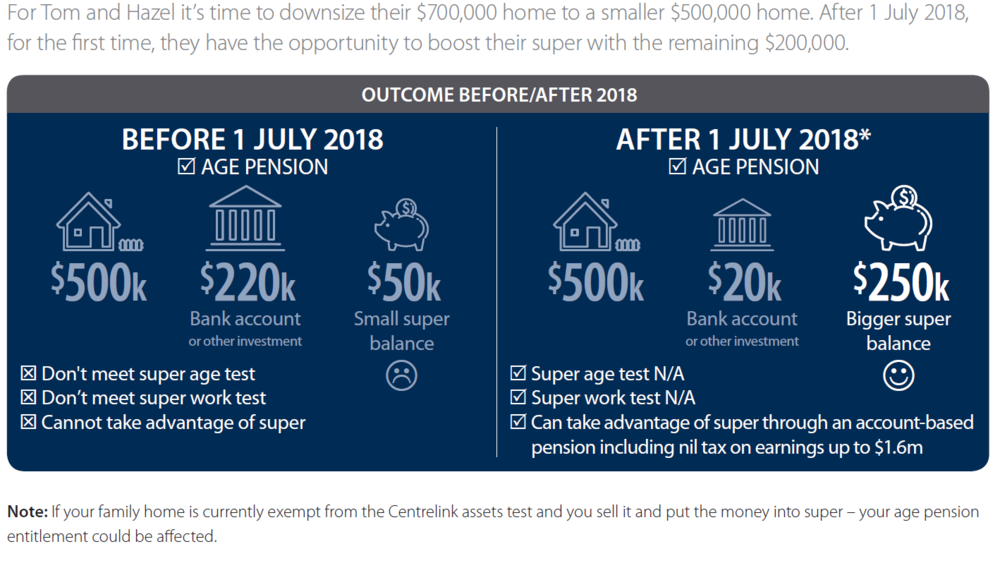

For example:

If this is of interest to you, please contact us to discuss your individual circumstances.

Disclaimer: This article is not legal or personal financial advice and should not be relied on as such. Any advice in this document is general advice only and does not take into account the objectives, financial situation or needs of any particular person. You should obtain financial advice relevant to your circumstances before making investment decisions. Where a particular financial product is mentioned you should consider the Product Disclosure Statement before making any decisions in relation to the product. Whilst every reasonable care has been taken in distributing this article, Australian Unity Personal Financial Services Ltd does not guarantee the accuracy or completeness of the information contained within it. Any views expressed are those of the author(s) and do not represent the views of Australian Unity Personal Financial Services Ltd. Australian Unity Personal Financial Services Ltd does not guarantee any particular outcome or future performance. Taxation Information in this document should not be relied upon without seeking specialist advice from a tax professional. Australian Unity Personal Financial Services Ltd ABN 26 098 725 145, AFSL & Australian Credit Licence No. 234459, 114 Albert Road, South Melbourne, VIC 3205. This document produced in August 2018. © Copyright 2018

{kind=link}