The 2026-27 Federal Budget Has Landed — Here’s What You Need to Know

Treasurer Jim Chalmers handed down the Albanese Government’s fifth Federal Budget on 12 May 2026, and it’s one of the most consequential in recent memory. With sweeping changes to capital gains tax, negative gearing, discretionary trusts and personal tax offsets, this Budget will directly affect how Australians earn, invest, and plan for retirement.

If you’ve been following the housing affordability debate, Tuesday night’s announcements won’t come as a complete surprise. But the full scope of what’s changing — and more importantly, when it takes effect — deserves a careful look before you make any financial decisions.

The Big Picture

The centrepiece of this year’s Budget is a two-pronged attack on property investment tax concessions, paired with new relief measures for everyday workers. From 1 July 2027, the long-standing 50% capital gains tax (CGT) discount on assets held for more than 12 months will be scrapped and replaced with inflation-indexed cost base calculations and a 30% minimum tax on net capital gains. This applies to property, shares, and most other CGT assets.

Simultaneously, negative gearing — one of the most hotly debated tax strategies in Australia — will be restricted to newly built residential properties only. Investors who purchased existing properties before Budget night retain their entitlements, but anyone buying an established residential property from 7:30pm AEST on 12 May 2026 will eventually lose the ability to offset those losses against other income.

On the upside for workers, a new permanent Working Australians Tax Offset (WATO) of $250 will be introduced from 1 July 2027, while a $1,000 instant tax deduction for work-related expenses kicks in as early as 1 July 2026 — no receipts required.

Who Wins and Who Loses?

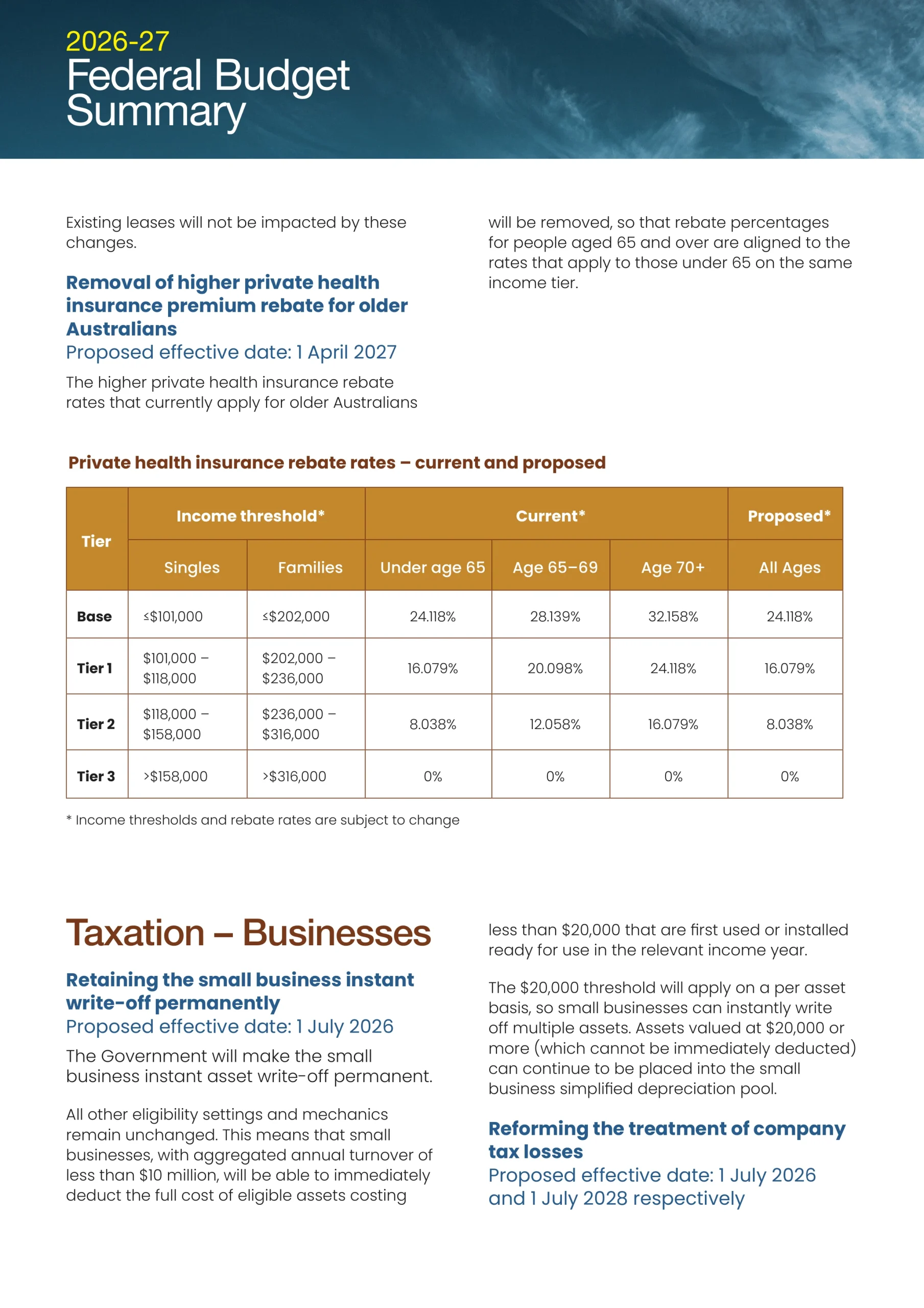

The winners include wage earners, first home buyers, small business owners (who gain a permanent instant asset write-off), and startups. The losers include existing property investors, high-income earners using discretionary trusts, and older Australians who will lose their higher private health insurance rebate from April 2027.

Superannuation, notably, has been left largely untouched — a welcome reprieve after the Division 296 debates of recent years.

In the sections below, we break down every major measure in plain English, including the transitional rules you need to know before making any moves.

{kind=link}